Unless you’re an agent, you probably don’t think about car insurance until it’s time to use it or pay your premium. Even though your policy may not be a page-turner, it’s worth taking time to get to know your coverage. Understanding your car insurance and what it covers ensures you have the right plan. It’ll also help you avoid confusion after an accident.

In this chapter, we’ll look at the different types of liability insurance and explore optional coverages. If you come up with questions along the way, please contact us at David Pope Insurance, and we’ll be happy to help.

Your car insurance policy covers you and family members listed on the policy when you drive your car or someone else’s car with permission. Auto insurance plans vary, and the type of coverage you have depends on your policy and what you want.

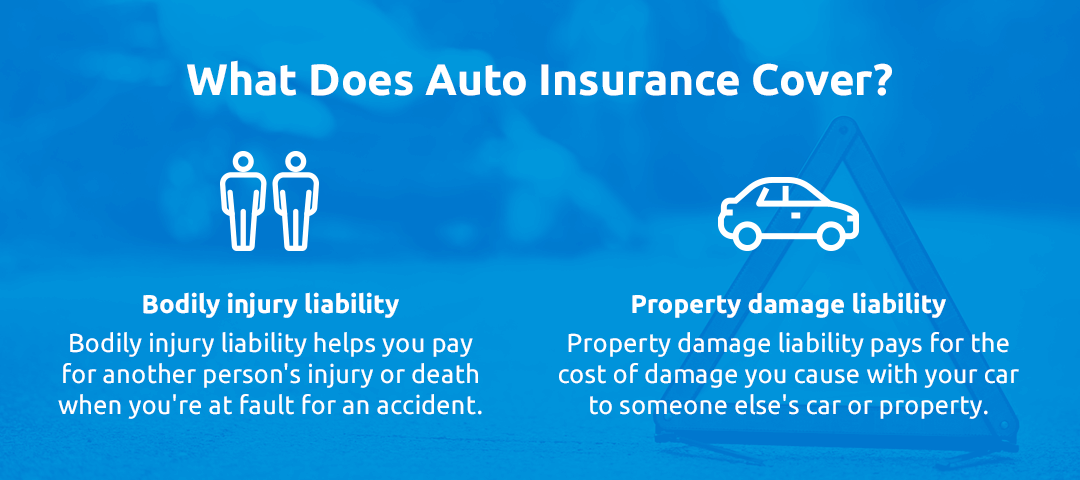

The type of coverage you need also depends on state laws and whether you’re financing your car and have a lender with certain requirements. Most states require basic auto insurance, which typically includes two types of liability:

Liability insurance may be available as either a combined single limit policy or a split limit policy. In a single limit policy, you will have one set amount covering both bodily injury and property damage expenses. For example, if you have a single limit policy that covers liabilities up to $200,000, that’s the most your insurance company will pay another party for injuries and property damage resulting from an accident you caused.

In a split limit policy, your coverage amounts are divided into three limits. For example, you might have $100,000 of bodily injury coverage per person, $300,000 to cover all injuries related to the accident and $50,000 for property damage. Overall, a single limit policy lets you apply coverage amounts as needed for an accident, while a split limit policy sets limits for you.

Get a Custom Auto Insurance Quote!

The amount of liability insurance you need depends on your state. In Missouri, motor vehicle owners are required to have the following liability coverage:

You can choose the minimum amount of coverage set by state laws or opt for a higher coverage amount. If the expenses related to the accident exceed your policy’s coverage amount, you will be responsible for paying for the extra costs. A higher amount will cover more of the other party’s expenses if you cause an accident, so there’s less chance you’ll have to pay out of pocket for anything. This is why some drivers carry more liability insurance than the minimum requirements set by their state. However, higher liability limits come with greater premiums.

Many states also require drivers to have medical payments coverage (med-pay) or personal injury protection (PIP) and uninsured motorist coverage. For example, in Missouri, vehicle owners must have $25,000 of uninsured motorist coverage for bodily injury per person and $50,000 for bodily injury per accident. While it’s not required to have PIP or med-pay in Missouri, it’s still a good idea.

You might choose the minimum amount of coverage needed to comply with your state’s laws and save money on your premium. However, if you can afford more, you have plenty of additional options to enhance your policy and increase your financial protection. These include:

Unstacked uninsured motorist coverage means you will receive coverage for an accident caused by an uninsured motorist up to the same limit you have set for your liability coverage. For example, if you have a $25,000 liability limit for bodily injury, that’s the most you can expect to get for your own medical expenses in an accident with an uninsured motorist.

Stacking means combining your coverage limits across two or more vehicles on one policy or across multiple policies in your name. Generally, you cannot stack property damage liability — only uninsured or underinsured motorist bodily injury coverage.

Stacking is the old way of doing things, and it costs more than unstacked coverage. It’s also not allowed in every state, and some insurance companies do not allow it even if it’s legal in their location. Most carriers are not happy with multiple cars in a household being on multiple policies. People usually put all of their household’s vehicles on a single policy and raise their limits if they want more coverage rather than stack limits.

Unless you review your car insurance policy daily, it may be easy to forget what coverage you have and what it means. For example, maybe you can’t remember if you signed up for comprehensive or collision coverage. Comprehensive and collision often go hand in hand, but they protect you financially in different ways.

Collision insurance covers your car’s damage if it’s involved in a crash with another vehicle or object. For instance, you might use collision coverage in the following situations:

Comprehensive insurance covers damage to your car that doesn’t involve a collision with another vehicle or stationary object, and may be related to the following:

If a rock hits and breaks your windshield, for example, comprehensive insurance may pay for the damage up to the limit in your policy. If your car is a total loss due to damage or theft, comprehensive coverage should pay the actual cash value of your vehicle. Actual cash value is the amount needed to replace your car minus depreciation.

It’s worth noting that both types of coverages have deductibles. So, say your car is worth $14,000, and you have comprehensive insurance with a $1,000 deductible. If your vehicle is destroyed in a fire, you will receive $13,000 from your insurance company to replace your car.

Many times, if you want to have collision insurance, you’ll also need to purchase comprehensive coverage. Neither of these coverages is required by law, but they might be mandatory if you have a car loan. Even if they’re not required, you might want to add comprehensive, collision or both to your policy if you can’t afford to buy a new car after an accident, or if you’re concerned about your vehicle being destroyed in a natural disaster.

If you have liability, comprehensive and collision insurance, you have what’s called a full-coverage policy. A full-coverage policy will have a higher premium, but it will also offer greater financial protection in an accident.

Not every person needs a full-coverage policy, but in some cases, it makes sense. Experts recommend choosing enough coverage to equal the total amount of your assets. Unless you do not own a home or other assets, you should select liability coverage of at least $100,000 per person or $300,000 per accident. Overall, you’ll want to think about all of the assets you have that you wish to protect and how much insurance you can comfortably afford to offer that protection level.

Also, consider the value of your car. If your vehicle is worth less than $5,000, for example, you may not feel it’s worth it to pay for comprehensive and collision coverage. However, this also depends on your needs, and you shouldn’t necessarily skip collision and comprehensive insurance just because you have an older car. If you don’t have savings to replace your vehicle in the event of an accident, it may be worth having a full-coverage policy, even if your car doesn’t have a high value.

Still not sure what you need? Continue onto the next chapter, or request more info at David Pope Insurance, and we’ll recommend a policy based on your budget and unique requirements.