Buying a new car is a big financial decision, and the process of finding your next vehicle may feel overwhelming. Part of finding the right car and doing your research is knowing which common car-buying questions to ask when buying a used car or new car from a dealership and knowing when is the right time.

Below, we include some questions to ask of all the parties involved, including your dealer, lender and insurance provider. Though this is not a comprehensive list, these car-buying FAQs are a great starting point when you are looking to buy a car.

Many car buyers feel intimidated at the prospect of buying a new car. You want to ensure you know what you’re getting and that you are making the best financial decision. Ask the following questions when buying a new car or a used car from a dealer to ensure you are getting the best deal for your budget.

Ask whether the dealer has serviced the car and when it was last serviced. Vehicles that sit in a lot for a long time can develop unseen issues. You should know when the dealership’s mechanics last looked at the vehicle and request that a copy of the service records be included in your car when you purchase it.

The maintenance history may not be included in the vehicle history report. This is why it is essential to ask the dealer directly about maintenance history that may be more difficult for you to find on your own. In fortunate circumstances, the vehicle may come with a maintenance log or with receipts that track the service that was performed on the vehicle.

In less fortunate circumstances, the maintenance history may not be as clear. Before you purchase the car and drive it off the lot, you may want to have the dealer perform any required maintenance and have a third party inspect the vehicle so you know what shape it’s in.

Too often, drivers purchase a car and drive off the lot without knowing anything about the warranty coverage. Maintenance costs can be expensive, so understanding how much coverage your warranty offers can save you a significant amount of money in the long term.

Warranties differ based on the model and year of the vehicle and the car manufacturer. Ask the dealer to review the details of your warranty coverage with you, including any possible exclusions. Doing so will give you a better understanding of what vehicle repairs you will have to pay for and what repairs will be covered under your warranty. You should also know how long your warranty is good for.

While you are discussing the car with the dealer, you may want to try negotiating the price. When you ask the dealer if this is the best rate they can give you, you’ll show you are interested in only the best rates. It is common for dealers to lower the price of a car to better fit your budget, and you can do your research beforehand so you have some leverage when you try to negotiate the price.

Ask what the actual, final price is for the vehicle. This cost goes beyond the car’s sticker price and includes all the fees. Dealers frequently charge fees for delivery and documentation, for example. All these costs should be listed in the purchase agreement. Ensure you understand every cost and ask the dealer questions if something confuses you.

For example, if the purchase agreement includes a fee for accessories, ask what this fee is for specifically. If the fee is for a clear coat on the vehicle’s paint to protect it from insects, you should be aware of this, as you may want to negotiate add-on services that you don’t want.

If you are purchasing a used vehicle, one crucial question you should ask is where the vehicle came from. Used vehicles often come from other dealerships, auctions and trade-ins. If you can access the vehicle’s accurate maintenance history, you may be able to spare yourself trouble in the future.

If the car is used, it may have been purchased at an auction. In this case, you may be able to obtain the vehicle records from a reporting agency like Carfax. If this report is not available, check where the vehicle was registered. This is important to know, as you may want to avoid purchasing vehicles from certain areas of the country, such as locations that recently experienced a hurricane or flood. After sustaining flood damage, a vehicle could have unreported electrical or mechanical damage.

Ask if the vehicle has ever been involved in an accident, if the dealership performed repairs on the vehicle and if any recent work was done. The answers to these questions can help you understand what you can expect for future upkeep and your safety in your vehicle. If you cannot find the vehicle history report online, you can request it from the dealership.

After you find your new vehicle, your next step is to secure financing. To do so, you may want to speak with multiple auto lenders that can offer the best rates and terms available to you.

One of the potential new car questions you may want to ask is how your credit score will influence your interest rate. A lower credit score may lead to fewer lenders willing to finance your vehicle and higher interest rates. Prior to shopping for your next vehicle, you may want to check your credit score and try to increase your score if it is less than stellar.

Borrowers with scores that fall in the nonprime, subprime and deep subprime ranges are often offered loan rates that are much higher than borrowers with prime or super prime scores. Your lender can advise you further on where your score falls and what rate you may qualify for.

Before you sign the paperwork for your auto loan, ask what rates are available to you and whether your interest rate could ever change. Compared to dealers, a credit union or your personal bank is most likely going to have the best rate available.

If the dealer is offering to finance your vehicle, you may want to walk away and consider all your options before you make your decision. Ask if you can place a deposit on the vehicle to hold it while you look into other financing options.

How much interest you pay over the course of your auto loan will be influenced by your interest rate and your loan term. Typically, loan term options for vehicles are expressed in months. While a longer loan term can give you a lower monthly payment, you will pay more in interest over the course of your loan. With a shorter loan term, you will pay more each month, but you will also pay less in interest.

Your loan term can impact your total cost by hundreds or even thousands of dollars. For example, if you buy a car for $30,000, put $5,000 down and are given an interest rate of 4%, if you choose a loan term of 48 months, your monthly payment will be $564 and you will pay a total of $32,095 over the course of your loan.

If you instead choose a loan term of 72 months, your monthly payment will be just $391. However, you will pay a total of $33,161 over the course of your loan. A longer loan term could also mean your vehicle is worth less when you pay it off as a result of depreciation than if you had paid it off faster. You may want to consider that a lower monthly payment with a longer term could allow you to pay off other high-interest debt.

Whether you should select a shorter or longer loan term depends on your specific financial circumstances.

If you will be financing your vehicle, you may want to ask what your down payment should be. The amount you pay upfront on your vehicle will determine what size loan you need and how much you will pay on your loan each month.

If you do not have much saved for a down payment or you are currently prioritizing other financial goals, such as saving for a house or retirement, you may want to have a smaller down payment or avoid a down payment entirely. Of course, putting down less upfront may mean you pay more into total interest and higher monthly payments.

For example, if the price of your car is $30,000 and your loan term is 5 years at an interest rate of 4%, your monthly payment with a $5,000 down payment would be $460. If you opt for a larger down payment of $10,000 instead, your monthly payment would be $368 and you would save a few hundred dollars over the course of the loan.

Consider what down payment amount will work for your financial situation, and include the other expenses that come with car ownership to determine what you can actually afford.

If your income has increased or you have paid off a high-interest debt, you may find you have more disposable income every month. As such, you may want to pay off your car loan early. Whether you can pay your loan early without incurring a penalty depends on the laws in your state and your contract.

To be charged a penalty for paying your loan off early, your contract should include a prepayment penalty clause. Speak with your lender about prepayment penalties before you sign an agreement. Even if you do not expect to pay off your loan early, this is good information to have if your financial situation changes in the next few years.

Along with the cost of buying your next vehicle, consider the cost of insuring your vehicle. There is more information you may want to gather from your insurer beyond how much coverage will cost. When you speak with your provider, ask the following auto insurance questions:

In some situations, a similar vehicle model can get a very different auto insurance rate. For example, a 2015 Dodge Ram pickup may cost hundreds of dollars less per year to insure than a Ford F-150 in the same location. When you add up this cost across the years you will own the vehicle, you may find a comparable vehicle will be significantly less costly to insure.

You can easily compare different models online, but you may also want to ask insurers directly about quotes for comparable models. Use these different quotes to determine whether you are purchasing a model that is affordable for you to insure or whether you want to go with a different model.

One of the questions to ask when getting car insurance is whether there are discounts and savings available to you. How much your insurance policy will cost can be influenced by the policy limits, coverages and deductibles you choose, along with your risk rating. Your risk rating determines your likelihood of making a claim. Various factors will also influence the cost of your premium, such as:

Though you may have no control over these factors, there may be discounts available that can help lower your premium. Your insurance provider may offer good student discounts, safe driver discounts, multi-car discounts, multi-policy discounts or continuous insurance discounts. Many insurers also offer discounts for paying your premium in full, by payroll deduction or via an electronic funds transfer (EFT).

Speak with your insurance agent to discuss which discounts are available and which you may be eligible for.

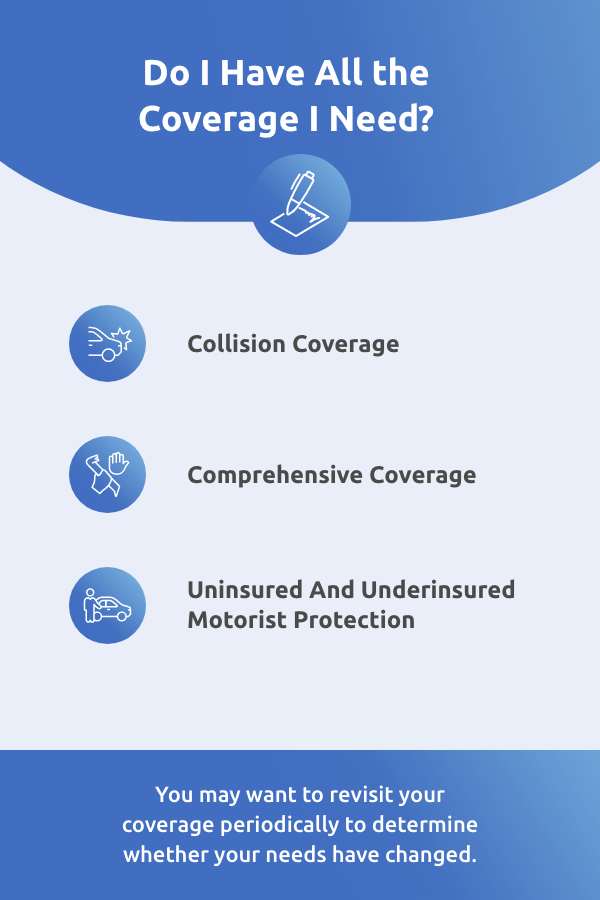

This is one of the most important insurance questions to ask, as you should understand exactly what forms of coverage you have and whether you have sufficient coverage. The state you reside in can impact how much minimum coverage you need. Many states require a minimum level of liability coverage, which will cover the cost of vehicle damage, property damage, death and legal fees in the event of a car accident.

After you are sure you meet the minimum coverage requirements in your state, ask your insurance representative what other coverage options may be best to meet your individual insurance needs. Many drivers should carry:

Your insurance agent can explain how the different types of coverage will impact your premium and what your out-of-pocket costs would be after an accident. In many cases, you may want to carry more than the state minimum coverage requirements. For example, if you have significant personal assets that you want to protect, you may want to purchase excess liability insurance. This is a separate policy that can help cover costs where your auto insurance leaves off.

You may want to revisit your coverage periodically to determine whether your needs have changed. If so, you may want to speak with your insurance provider about changing your coverage.

If more than one person will be driving your car, you may want to ask your insurance provider about who will be covered under your policy. Many married couples share vehicles or drive each other’s vehicles regularly. Couples with teenage children may also let their young drivers use their vehicles.

If this is your situation, you may want to bring this up when discussing your coverage needs with your insurance representative. They can help you figure out how much coverage and what type of coverage you need. Your insurance agent can also let you know how adding another driver to your policy will affect your rate. For example, if the other driver is a first-time driver, this could increase your premium.

You should know how much you can get from your insurance policy if your car is totaled in an accident. Ask whether you will receive the agreed upon value or the actual cash value:

After your car is totaled, the last thing you want to deal with is receiving a check worth much less than you anticipated. Knowing the numbers before an accident ensures you know what to expect.

At David Pope Insurance, we serve those seeking personal and commercial insurance in Missouri, Kansas, Tennessee, Nebraska, Illinois, Arkansas, Colorado and Iowa. We can offer you a customized, affordable policy that meets your unique insurance needs and circumstances. Your new vehicle will need auto insurance, and this can be a great opportunity to switch insurance for increased savings.

We represent leading providers to ensure we can deliver you high-quality, budget-friendly insurance policies. Contact us at David Pope Insurance to learn more about insuring your car, or request a quote from us today.