While you may have enjoyed living in your apartment, you’re ready for a change. Maybe you want a yard for your dog to run around in, or perhaps your family is growing and you need more space. An office and a garage could also be nice perks. A home can offer you more space, and it can also be a significant financial asset and investment in your future. However, you may not be certain whether you are ready to make the move. What do you need to know before buying a house? How do you know if you’re ready financially?

Being in control of your finances early on in your move is especially important. Fortunately, based on your rental insurance agreement, you may be able to qualify for cheaper home insurance. As such, it is important to be in contact with your insurance provider throughout the process to track and control the best deals and ensure everything is getting done.

Moving from an apartment to a home will affect your insurance plan, and whether you rent or own, your property and belongings should be protected by the proper insurance. To help you through the process, we’ve compiled this guide to moving from an apartment to a home that covers the most important things to know before buying a house.

The first step is figuring out if it is time for you to move from an apartment to a house. Before you make the decision to move, you will need to consider your budget, location and stress level, along with the process of transferring all your belongings and potentially paying people to help you. If relocation is the right decision for you, any challenges you face will be worth it.

For many first-time homebuyers, the following are some common reasons to move from an apartment to a house:

Have you found the city or small town of your dreams? If you are settling down in an area, buying a home can end up being cheaper in the long run. Along with being an affordable option over the long term, buying a home contributes to your net worth. As a renter, you are technically growing your landlord’s net worth.

With the expansion of a family, the need for more space often also means searching for a home. If you have added a couple of children or pets to your household, you may be considering an upgrade to a house as the next logical step. In addition to wanting more space, there may be other aspects of a home that could make it a better option for you, such as:

Even if you don’t have children, buying a home in a great school district can be a big bonus when you are ready to sell in the future.

If you have the budget for a new home, are tired of apartment living and are looking for more freedom, a new home may be your best option. For some homebuyers, apartment living doesn’t allow them to live out their dreams. Maybe you want more luxury in your home, such as a big kitchen, a huge master bedroom and a bathroom with a rainfall shower and a towel warmer.

Beyond the luxurious, your apartment may not include basic amenities like a washer and dryer. Imagine being able to wash and dry your clothes in your own home. Tired of listening to your neighbor’s loud TV every night while you’re trying to sleep? You can say goodbye to these nuisances when you’re a homeowner.

When you are a homeowner, you will likely have more freedom than you did as a renter. When you rent an apartment, you can be subject to the whims of your landlord. You may be restricted in the improvements and renovations you can make, or you may have to pay extra to have a pet. As a homeowner, you can redecorate, replace the carpeting and paint the walls any color you want. As long as you have the budget for it, you can make whatever changes you wish to your home.

New homes can be a great investment if you take care of them and aim to buy low and sell high later on. Your property may increase in value over the years, and the value of this asset can be a large part of your net worth. Moving now may also be the right option for you financially if:

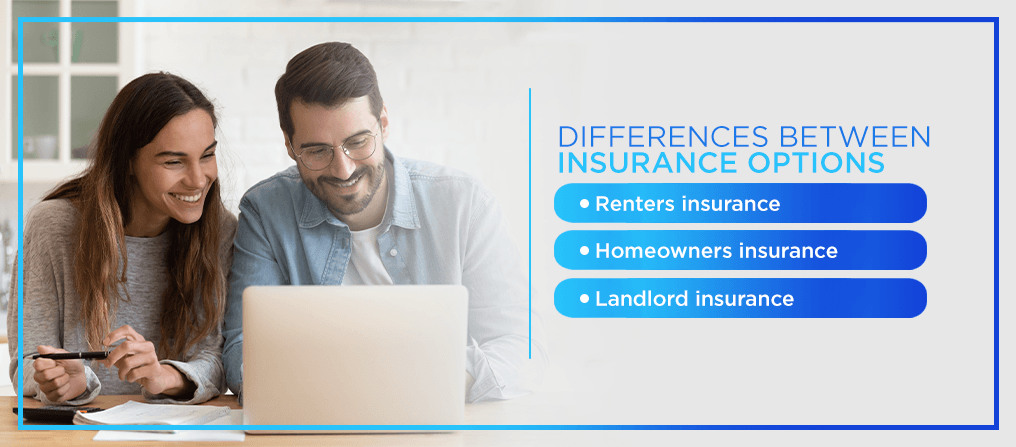

When moving from an apartment to a home, you may want to consider the differences between insurance options, the price differences between renters and homeowners insurance and potential hidden extra costs:

As a renter, you likely already have renters insurance. Similarly, you need to consider the type of insurance you will need to get if you are moving to a new home. As a homeowner, you will need homeowners insurance, and you may also want to purchase landlord insurance depending on your situation:

What happens to renters insurance once you decide to move to a home? When you move, you may want to wait to cancel your renters insurance, as this insurance could provide coverage for your belongings during your move. After the move is complete, you may then want to cancel your renters insurance policy.

What is the price difference between renters insurance and homeowners insurance? Because homeowners insurance covers both your belongings and the physical structure of your home, you will typically pay more money for a homeowners insurance premium. As a renter, you do not need insurance for the building itself. Instead, your insurance needs to cover only your personal belongings.

On top of insurance, what other hidden costs should you be aware of as a new homebuyer? As a homeowner, you may also need to pay property taxes, HOA fees and fees for optional services:

There are other types of insurance you may also want to look for as a new homebuyer that could present additional costs for you:

Once you have decided you want to move into a home, you may be wondering what you should do about your finances and insurance, how soon you need home insurance and if you have other options. The following are important steps to take and keep in mind during the transition process:

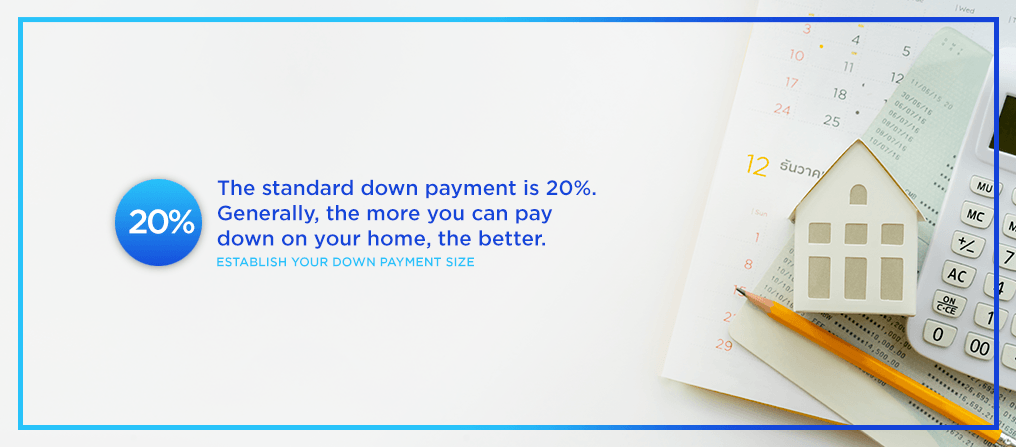

The standard down payment is 20%. Generally, the more you can pay down on your home, the better. Your mortgage will be a smaller amount, and therefore, you will also pay less in interest over the life of the loan.

However, you can still purchase a home with little to no down payment. If you are unable to save anything for a down payment, this can be a sign that you may not be ready to be a homeowner. Expenses like your mortgage, insurance and taxes are just the start of your costs for homeownership. You will also need to be able to cover costs for maintenance and repairs.

To determine the best amount for a down payment, you may want to speak with your financial advisor and lender.

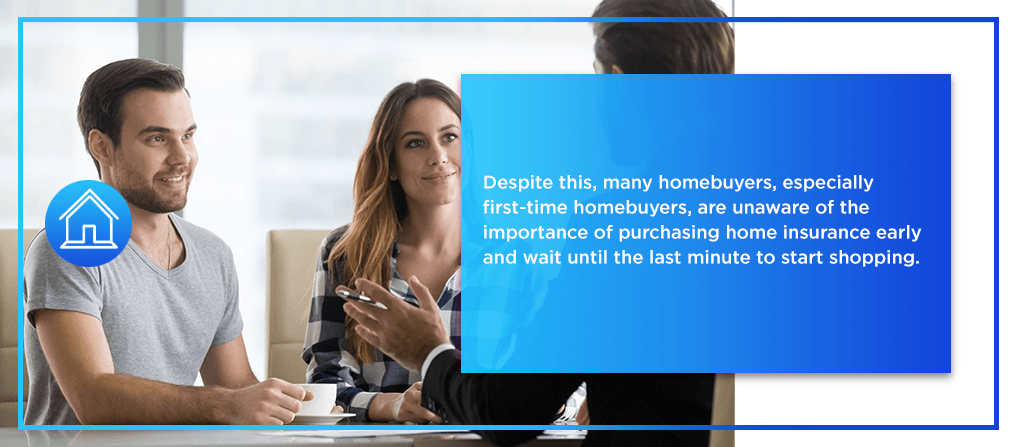

Many insurance companies want evidence of homeowners insurance before you close on a new home. Despite this, many homebuyers, especially first-time homebuyers, are unaware of the importance of purchasing home insurance early and wait until the last minute to start shopping. If you do not have insurance on time, your closing could be delayed. The earlier you start, the more time you will have to compare the different companies and coverage options available to you. You will also ensure that you are able to close and move in on time.

Keep in mind that home insurance is meant to cover major losses. You may still want to cover minor problems out of your own pocket. Think of home insurance as your coverage for catastrophic losses rather than as a maintenance fund.

For example, if you notice a minor roof leak, you may choose to file a claim. Next year, you may need to file a more expensive claim for your kitchen. While your homeowners’ insurance may cover both claims, your premium may increase. And if you file another claim within the next few years, your policy may not be renewed. When you face nonrenewal, you will need to find another insurance company to provide your coverage, and this company may charge more due to your claims history.

This is especially important to keep in mind when you are insured by a new company. Small claims filed with a new provider can lead to greater financial problems than what you would experience fixing a minor roof leak on your own. To help you determine which claims are worth filing, select the deductible that is right for you. Choose the highest deductible you can comfortably handle, and file a claim only when an issue is more expensive than your deductible.

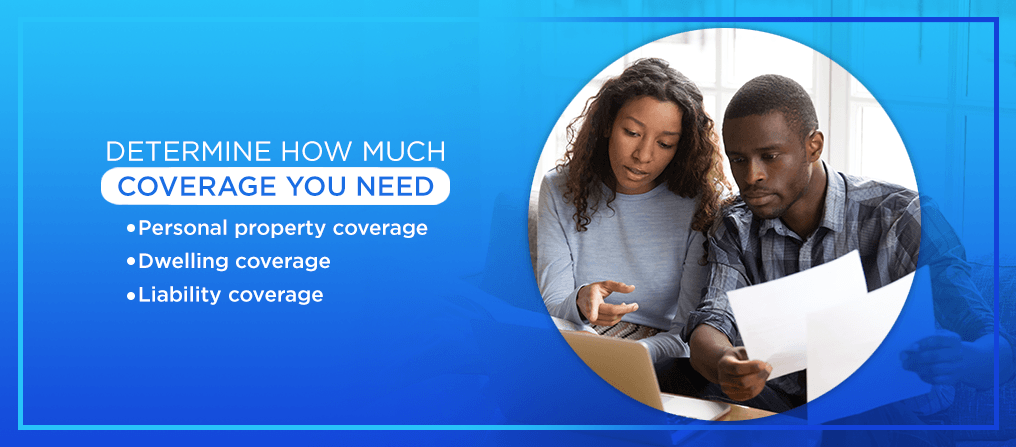

Finally, you may also want to determine how much coverage you need under your homeowners insurance policy. Your options may include:

Your home is one of the biggest investments you will make in your life, which means you should be adequately insured to protect this valuable asset. If you are unsure how much coverage you need for your specific circumstances, consult with the insurance experts at David Pope Insurance Services, LLC.

If you have more questions about moving from an apartment to a home, check out the answers some frequently asked questions below:

If you haven’t been budgeting, now is the time to start. Before you take on a financial responsibility as large as homeownership, you should know exactly what your income is and how much you spend on a monthly and yearly basis. Being familiar with your finances will allow you to determine how much home you can afford. If you have low debt or no debt, this may be the ideal time for you to become a homeowner.

It may seem premature to consider how long you plan on staying in the area where you will be buying a home, but this is a consideration that could have an impact on you financially. The longer you stay in your home, the more you will be able to pay off on your mortgage. You will be building equity in the home, and you may be able to pocket more of the money when you eventually sell.

Affordability is an important consideration when you are determining whether to move and where. You may want to prioritize living within your means and living comfortably, and this goes beyond your costs for housing. Affordability also includes the cost for food, taxes, gas and utilities. If you have been struggling to get by in your current location, you may want to consider moving to a more low-cost market.

To determine how much home you can comfortably afford, you may want to pinpoint what your typical monthly and annual household income is. What monthly payment can you afford? Plug this number into your budget and calculate how much you can afford to pay in total each year.

Do you have all the insurance coverage you need, or do you need to purchase additional policies? As a homeowner, you may need:

If you need insurance plans, you may want to consider an umbrella insurance policy. This is a low-cost way to carry a large amount of additional liability coverage.

If you are looking for home insurance in Missouri for you and your family, let David Pope Insurance be your one-stop shop. We are a local, family-owned insurance provider with the insurance services you need. When you choose David Pope Insurance, you can enjoy advice from an expert, significant savings, flexibility in coverage terms and exceptional customer service. We promise quality of care and the best pricing.

We aim to find you insurance options quickly. Rather than waiting days for a response, you can have information in a matter of hours. If you have unique insurance needs, we want to hear about them and work with you to figure out the best possible solution.

Are you seeking homeowners insurance as you move from an apartment to a home? Request more information or a quote from us today. You can also contact us to set up an appointment online.