No one wants to ever get into an accident, especially not one that causes severe damage to their vehicle. However, you should still plan for such an unlikely event. The first step is to know how your car insurance payout works. By better understanding this aspect of your insurance policy, you can set a realistic expectation of how much you can receive and when you’ll get paid if you have a wreck that totals your car.

Here’s a quick overview of how car insurance companies pay out claims: First, your payout claim must be approved. This can take around 30 days, but can vary depending on the insurance company. Next, the car insurance company will mail a check or set up a direct transfer of cash to your bank account. Finally, if you disagree with the payment amount, you can find options to negotiate with your insurer.

Learn more about car insurance companies pay out claims below.

Accidents usually create minor to moderate damage to the vehicles involved. This type of harm only requires repairs that cost less than the value of the car. If this happens, your insurance or the other driver’s insurer pays for covered repairs. How much and whether your insurance pays is based on who was at fault for the accident and the type of coverage you have. Most people only encounter this simple form of auto insurance coverage, however, payments become more complex when a vehicle sustains severe damage.

However, when the car becomes unrepairable or the cost to fix it would exceed a set percentage of its value, you could qualify for a totaled car payout from your insurance, depending on your policy. The type of coverage that pays for a total payout comes from the cause of the accident or damage. If you want coverage in the event that you need a car insurance payout, you should have collision or comprehensive coverage on your vehicle. In cases where another insured driver was at fault, their insurance should cover the payout amount.

With a totaled car payout, the insurance company determines the value of the vehicle before the accident with their appraiser and a third-party assessor to find a fair value. The value determined does not cover the cost to replace your totaled vehicle with a new model like it. Additionally, it does the value guarantee that it will equal any remaining car payments you may have on the vehicle. These types of payments require special add-ons to your policy.

For cases in which the car may require costly repairs, your insurance company may declare the car a total loss if the repair costs exceed a percentage set by the insurer or the state. For instance, in Missouri, if the cost to salvage and repair the vehicle exceeds 80% of the actual cash value, insurers must consider it a total loss and provide a payout for covered vehicles.

Car insurance payouts have several factors that determine whether a person gets a payout and how much. These factors are specific to your insurance policy. Therefore, you need to make sure to carefully read everything in your specific auto insurance policy and talk to your insurer if you have questions to find out more about your car payout coverage.

You need to know your insurance policy’s maximum limits. This amount is the greatest value the company will pay you for replacing your vehicle. Any insurance you have should cover up to the value of your vehicle to ensure that you can get a full payout. Discuss coverage amounts with your insurer, especially if you get a new vehicle or make significant upgrades to your existing one. You will find all information about policy limits for various incidents in the declarations page of your insurance policy.

Explore Auto Insurance Options

How much insurance pays out derives from whether you have a total or partial loss. Partial losses look at the cost to repair the vehicle rather than pay for its actual cash value (ACV) before the accident. However, when the repair costs are higher than a percentage set by the insurer or their state, the partial loss becomes a total loss.

For instance, Missouri has an 80% limit on repair costs before the vehicle is a total loss. Hence, if you live in Missouri and have a vehicle with an actual cash value of $50,000 that would cost $40,000 to repair, your insurance will consider it a total loss because $40,000 is 80% of $50,000.

Total loss claims happen when the car is beyond repair. The amount of money that you get from a total loss comes from the actual cash value of the vehicle. This value also is how insurers determine payment for partial losses.

Replacement value and actual cash value are two different ways of assessing and paying for a totaled vehicle.

The ACV is not the cost of replacing your vehicle with a new car because it takes depreciation, mileage, cosmetic damage, local demand, mechanical issues, make, model, year, accident history and other factors into consideration. Therefore, the ACV determined by the insurance company will be less than you spent for the vehicle. Often, ACV is the amount used for collision or comprehensive coverage to pay for a totaled vehicle. If another person caused the accident, their insurance would cover this cost.

Replacement value is the amount you would need to buy a vehicle similar to the one that sustained damage. Consequently, it is often much higher than ACV. Since comprehensive and collision coverage don’t include this amount, you may want to look into gap insurance or replacement vehicle coverage. The former covers any costs if you still owe money on a financed or leased vehicle. The latter covers the replacement value if you total your vehicle.

The type of vehicle you drive and your driving needs will help you and your insurer find the best coverage to get ACV or the replacement value for your vehicle in an accident.

If an accident investigation from your insurer finds that you were at fault, you would only have a payout for your totaled vehicle if you carry collision coverage. This type of insurance covers damage to your vehicle in a collision, regardless of whose fault the accident was. Your insurance company may sue the other driver’s insurer to get compensation for payments it made if the other driver was at fault.

Comprehensive coverage pays for damage from causes other than collisions. Examples of incidents comprehensive coverage may pay for include fires, natural disasters and vandalism. So, if a tree falls and totals your vehicle and you have comprehensive coverage, your insurance company will provide a payout.

Most people carry liability as required by most states. However, a myth is that only having this type of coverage is cheaper in the long run. But, having liability-only insurance means that if your vehicle gets totaled due to an at-fault accident or from weather or vandalism damage, your insurance company won’t pay. Therefore, if you cannot afford to replace your vehicle, liability only could be even more costly.

For instance, even if you have an older vehicle or one that is only worth $3,000, you should still consider adding comprehensive or collision coverage to your policy. With these types of coverage, you won’t have to pay for a new vehicle yourself if yours gets totaled. The lower value of your current vehicle means these coverage options will have lower deductibles or payments than if you owned a $50,000 vehicle.

If you got into an accident that totaled your vehicle and the other driver was at fault, their liability insurance coverage should pay for the damages. The limits on their policy and their insurer’s valuation of your vehicle will both play into how much you can get from a payout.

Different states have varying laws governing insurance payouts. For example, some states have requirements for the threshold for repairs that insurers can use to determine if they declare a vehicle a total loss. Other states may have requirements about liability coverage or require taxes and fees for replacing your vehicle to be included in the payout. Talk to your insurer to get the right coverage for where you live.

How the accident occurred is also important. Whether you, another driver or a non-collision event caused damage to your car decides which type of insurance will cover the payout. In a non-collision event, you must have comprehensive coverage for your insurance to pay for your totaled vehicle. For an accident that was the other driver’s fault, their liability insurance should pay. However, if you were at fault, you would need collision coverage to ensure that you get paid.

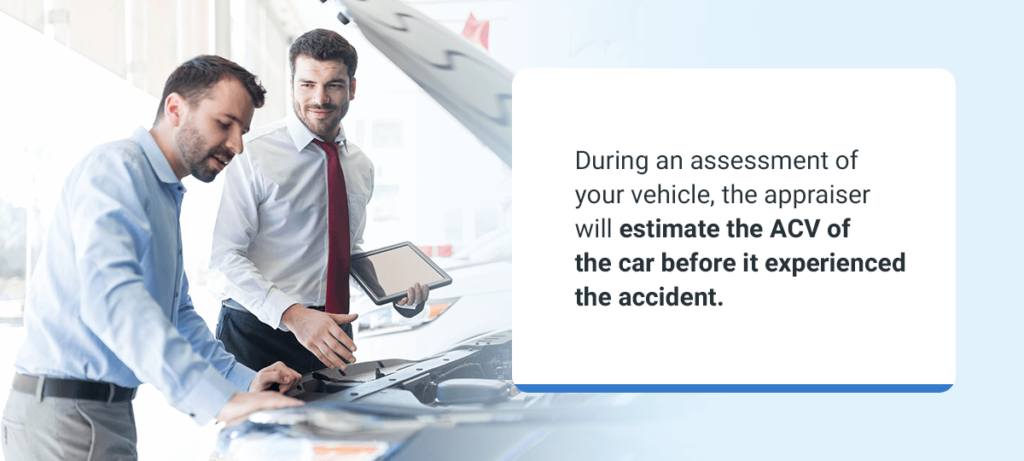

When calculating your totaled vehicle payout, most insurers use the actual cash value of the car. This is not the replacement value. You must have separate coverage for that higher amount. The actual cash value comes from a complex calculation that starts with your insurer’s appraiser. During an assessment of your vehicle, the appraiser will estimate the ACV of the car before it experienced the accident.

Some things that can impact the ACV and make it lower than the replacement value include your car’s mileage, age, make, model and any existing wear or damage to it. Depreciation makes a significant impact on the ACV. As soon as you leave the car dealership with a new vehicle, it loses value. This loss is included in calculations for ACV, which is why it is often thousands of dollars lower than the replacement value for a vehicle of the same year, make and model.

While keeping your vehicle well maintained and having a record of no accidents won’t significantly raise your ACV, it will help to keep it from dropping too much due to vehicle damage or problems.

By using the ACV instead of the replacement value, insurance companies can save money and pass those savings onto their customers. However, you are always able to request coverage for the replacement value if you want to get a new car of the same make, year and model as your current one.

After the cash value is calculated, how does the insurance company payout the claim? Once calculated, you may not get the full payout immediately — you must agree to the amount with the insurer. You will also need to provide proof of sale and the title to the car.

If you want to dispute a too-low figure, you have the right to do so. After you’ve agreed to the payout, your insurer will first pay off any remaining car payments or loans from the payout directly to the lenders. Therefore, you may not receive any cash from the payout if your payout was less than or equal to the amount you owed for your car. If the payout does not fully cover the remaining balance on your loan, you will have to pay for that out of pocket — unless you have gap coverage.

Gap coverage is an add-on to your auto insurance that will pay the full amount of your loan or leased vehicle if your insurance payout does not cover the total cost. Since this coverage only adds a small amount to your premiums, it’s a good idea to get it when leasing a vehicle or during the early times of paying off a new car. Some leases may require that you have this type of coverage before you can acquire the vehicle.

After paying off your vehicle’s lease or financing from the ACV, minus your deductible, the insurer will give you the rest. You can use this toward buying a vehicle to replace the totaled one.

The time it takes for you to receive payment for a total loss may be much longer than you think. The insurer has to assess your vehicle’s damage and value. Plus, they need to get details about the cause of the accident and the other driver’s insurance. The entire process for the car insurance company to pay the claim may take 30 days or longer.

Some states mandate payments within a specific timeframe. For example, in Missouri, insurers have 10 days to acknowledge receipt of the claim. Then, they have another 15 days to decide on that claim. Following that, they must make a prompt payout without a specific timeline.

Delays in filing your claim or getting information from the other driver can delay the entire payout process. The faster that you get your side of the paperwork completed, the sooner your insurer can begin work on getting you a payout.

You will also want to have your vehicle towed to a mechanic’s shop approved by your insurance company after an accident. The mechanic who already works with your insurer can more quickly get them an assessment of the cost of repairs. The faster your insurer has this information, the sooner they can decide whether to declare the vehicle a total or partial loss.

Other factors that may delay your payout include a widespread natural disaster, such as a flood or tornado. Because local insurers will have their hands full with making assessments and payouts, it may take longer than normal to get your payout.

Poor communication with your insurer or the other driver will also delay the payment process. The insurance company needs a basic amount of information before it can proceed with the claim. Therefore, the longer it takes to get that information from the other driver or to your insurer, the longer your payout will take.

If you don’t have the cash to cover your deductible, you could also face a delay in getting your payout. Having a savings account to cover your car insurance deductible can reduce delays in getting your payment. However, you may also choose a policy with a lower deductible in exchange for higher premiums. Your insurer can help you find the right balance between premiums and the deductible based on your coverage, vehicle and finances.

The payment from the insurance company depends on the type of claim that’s been filed. If you are the one at fault, the check will eventually go to the other driver in the accident. However, if the other driver was at fault, the insurance claim payout goes directly to you or the body shop where you’re getting your repairs done, depending on the state.

The initial payout amount offered by your insurance provider may be much lower than you expected. There are several reasons that you may not agree to the amount that your insurance company will payout for your totaled vehicle.

One of the most common reasons for disagreement is not understanding what your insurance policy covers. Carefully review your policy to understand the types of coverage you have. You may not qualify for a payout if you have liability-only coverage and a natural disaster caused the damage. Alternatively, you may have expected replacement value when you don’t carry an add-on for this.

Another reason that you may not agree with the payout amount is if you added upgrades to your vehicle the insurance company did not know about or consider. For example, if you added a sunroof or had a new paint job, these might make the ACV higher than the appraiser determined.

Lastly, if you still had several payments on your vehicle and a special financing offer that reduced or eliminated the down payment, you might not get as much from the payout as you expected. In fact, if your payout covers only part of the amount that you owe, you would not get any money from the payout and still need to pay for the rest of the vehicle’s cost. Check your policy and get gap insurance to prevent this from happening.

While gap coverage won’t give you any money after it covers the remainder of your auto loan or financing, it will still keep you from having to pay for the rest of the cost of your totaled vehicle. If you disagree with the payout, you have options to negotiate with the insurance company.

In many cases, drivers don’t agree with the payout amount. If you find yourself in this situation, there are some ways to dispute the insurer’s payout. You will need to gather evidence to support your claim that your payout is too low and then send a counteroffer to your insurer.

First, if you made upgrades to your vehicle, gather receipts from those. Upgrades may include enhanced audio systems, a new paint job or a rebuilt engine. These could contribute to a higher ACV than what the insurer quoted.

Second, get an assessment from an independent appraiser. They may not agree with the insurance company’s assessor or the value determined by the third-party assessor the insurer also consults with.

Third, research the values for similar vehicles like yours. Consult the Kelley Blue Book for an estimated resale value of a vehicle with your make, model and year to get a better idea of how much your vehicle’s ACV might be.

Last, if you provide a counteroffer with the above information that the insurance company does not accept, you may want to consult with an attorney. In some cases, insurers may have made errors in inputting your information into their system. Some instances of unscrupulous companies falsifying policyholder information have also occurred. A lawyer might help you uncover such cases or help you negotiate a better payout.

Your car insurer makes a difference in what type of policy you have, how much you spend and how you get payouts. Choose a provider who will work with you and your budget to ensure that you get a policy for your vehicle that covers exactly what you need.

David Pope Insurance is family-owned with 20 years of experience in the industry. Request a quote for auto coverage today to see how much you can save on the comprehensive coverage that can provide a payout if needed.