If you’re taking out a mortgage for a new home, most lenders will require you to have an escrow account. Escrow involves setting money aside in advance for expenses like your homeowners insurance. This setup could be a little confusing if you’re unfamiliar with escrow accounts. This article will help you understand escrow and how you can find the best homeowners insurance to fund with it.

Escrow is an account that holds money during an ongoing transaction, like buying a home. It’s your money’s secure halfway house between you and the parties you need to pay for costs like your homeowners insurance, mortgage and tax payments. You could also consider it a savings account under third-party management for your expenses as a new homeowner.

From the escrow account, your lender ensures the right amounts go into the right accounts on time so you don’t miss any bills.

Paying for your homeowners insurance with your escrow account helps protect your home every month. It also assures the lender that their investment will be secured from mishaps while you pay it off.

You and your lender want the same thing — to keep your home safe while you pay it off and become its full owner. An escrow account helps keep your homeowners insurance fully paid for everyone’s peace of mind. The details of how this works will vary with your lender and the mortgage terms, but the following is a typical outline.

Your lender will open an escrow account for you or ask you to open one to close the mortgage. In addition to your mortgage payments, you’ll use this account to pay property taxes and sometimes other amounts, like homeowners association (HOA) fees. Most lenders require homeowners insurance, and many will expect you to pay these premiums into your escrow account.

To ensure your escrow account has enough funds to cover expenses, many lenders require you to pay your first year’s insurance premium in advance when you close your mortgage. After that, you’ll pay a monthly amount that contributes toward future premiums and taxes, as well as repaying your mortgage.

Your lender will distribute funds from the escrow account to pay these different expenses, including your homeowners insurance premium when it’s due. If your premium changes, your lender will credit the surplus to you or request that you pay in the shortfall.

There are several benefits to using an escrow account to pay your homeowners insurance:

While escrow accounts are helpful for homeowners insurance payments, keep the following facts in mind:

Beyond the basics, you may have more questions about escrow and home insurance. Here are answers to some of the most common questions to help you navigate escrow successfully.

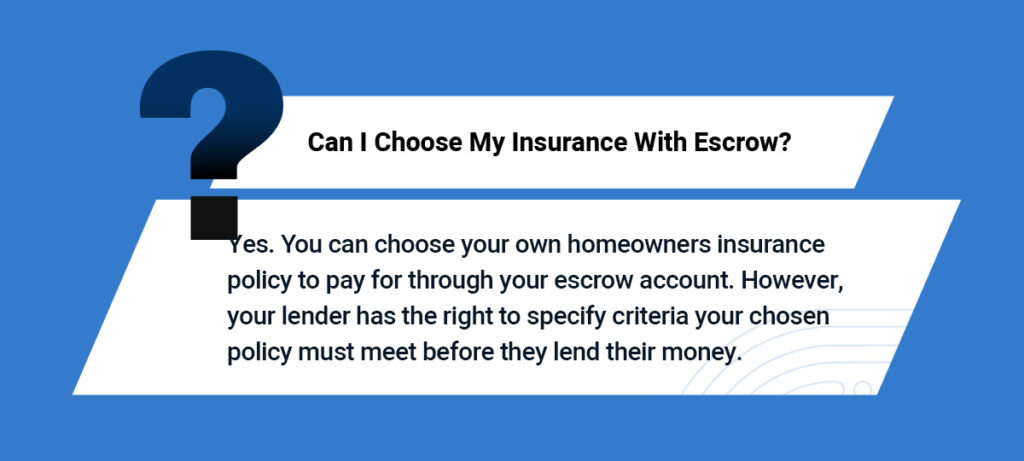

Yes. You can choose your own homeowners insurance policy to pay for through your escrow account. However, your lender has the right to specify criteria your chosen policy must meet before they lend their money. Check that you understand your lender’s requirements and explore policies that fit your priorities while meeting your lender’s standards.

Yes. If you’re already paying for homeowners insurance through your escrow but find a different insurance policy you prefer, you can switch by following these steps:

Many lenders require you to escrow your homeowners insurance payments. If you prefer not to, you could ask whether you qualify to opt out. They may allow this in some cases, such as if you make a larger down payment or show excellent credit.

Paying some or all of your first year’s homeowners insurance premium upfront ensures the escrow account has enough funding to start coverage immediately and maintain it for the year while protecting the lender’s investment.

Your lender may allow this if you ask for their approval. You may need to prove they can rely on you to manage the payments yourself.

Yes, as long as your homeowners insurance is included in your escrow and you have enough funds in the account. Your lender will use the funds in the account to make payments for you whenever they’re due.

You can stick with your current policy if you like it and it meets your new lender’s requirements. If you would prefer to switch, this is a good time to do so.

Your lender will close the account. If surplus funds remain in it, they’ll refund you. You’ll need to manage your insurance and tax payments after that.

Yes! Your home is now truly yours. Whether you see it as an investment, a place to rest your head or both, keeping up with homeowners insurance premiums protects your property and gives you peace of mind.

Are you buying a home in Missouri or a nearby state? Whether you’re taking out a mortgage and including homeowners insurance in your new escrow or you’re already insured and curious about better deals, David Pope Insurance will find you the best value coverage for your needs and your lender’s requirements.

David Pope Insurance is an experienced, family-owned Missouri insurance agency. We know homeowners insurance and deliver fast, flexible, custom quotes to meet your needs at the lowest prices. Tell us your lender’s requirements, and we’ll find you the best deals on policies that match them.

Request homeowners insurance quotes, and we’ll respond the same working day.