Understanding how much life insurance you should get can be tricky. Many factors go into determining the right amount of life insurance for you and your family. Below, learn how life insurance works and the common misconceptions about these policies to help you determine what type of policy is best for you and how to calculate how much coverage to get.

Life insurance is a policy that involves an insurance company paying a specified amount, called the death benefit, after the insured person’s death. You choose how much life insurance coverage you need and pay the premium to ensure the coverage amount is paid in full after your death.

The purpose of life insurance is to provide peace of mind that family and loved ones are financially protected after your death. A life insurance policy allows you to continue providing for your loved ones after death.

When seeking life insurance, you can generally choose from three main types of life insurance:

Whole life insurance policies are permanent policies, which means you’re covered for your entire life as long as you make the premium payments. These policies are the most common, as they offer the most stability.

Whole policies offer an investment component to build cash value on your premiums, which works like a savings account. You can eventually use these savings to pay your premiums or you can cash them out, which is subject to tax.

Whole life insurance tends to be the most expensive.

Term life insurance covers you for a fixed term, such as 20 or 30 years, with options for renewal. You can choose term lengths depending on age, health and coverage needs.

For example, you may get term life insurance now with the expectation you’ll build up enough assets that you won’t need a new policy after it expires. Term life insurance is relatively straightforward and often has more affordable premiums than other types of life insurance.

Universal life insurance is another type of permanent coverage. These policies typically offer the same benefits as whole life insurance while being more flexible.

In this case, the policyholder typically has some say in their rates and how the policy is split between cash value and death benefit. Other differences between universal and whole insurance include fluctuating rates and lower premiums.

Request a Free Life Insurance Quote!

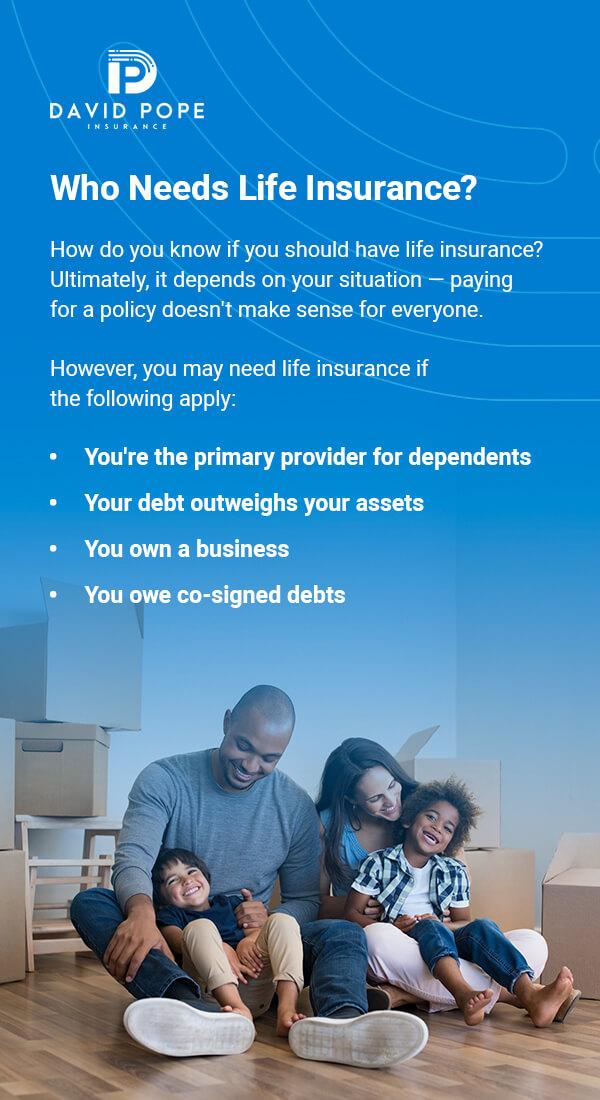

How do you know if you should have life insurance? Ultimately, it depends on your situation — paying for a policy doesn’t make sense for everyone. For example, suppose you’re single without dependents and have enough money to cover debts and death-related expenses, or you have enough assets to provide for dependents after death. In either case, you may not need life insurance.

However, you may need life insurance if the following apply:

Have Questions? Contact Us Today!

Many people are unsure about getting a life insurance policy because of the many misconceptions surrounding life insurance. However, life insurance should be viewed as a comprehensive tool and decision that allows you to manage life’s risks. Here are several common myths about life insurance and what the actual truth is.

This is one of the most common myths you’ll hear about life insurance, though it’s not quite true. You can get life insurance at any age.

The reason people say you can’t is that insurance companies will view you as more of a risk to insure as you get older because you’re naturally closer to death. Most insurance companies will still allow you to get a policy — you’ll just likely pay high premiums for it.

Many companies offer life insurance options, which can be great to sign up for. The misconception is thinking that this coverage is enough for your entire life.

Your employer will typically only cover your life insurance while you’re employed with them. Life insurance through your employer may be enough while you’re young and working, though if you leave or retire, you’ll be without coverage.

Usually, it’s best to supplement your employee insurance with a customized life insurance policy.

Life insurance is something you must buy before it’s needed. As a young and healthy individual, you’re doing yourself a disservice by thinking you don’t need life insurance.

While you can get a policy at any age after 18, purchasing life insurance while you’re young and healthy is a great way to lock in low premiums for comprehensive coverage.

The cost of life insurance depends on numerous factors, and there are many ways to get an affordable policy. For example, start your policy young or start with a term policy until your budget is higher. You can also work with your insurance company to create an affordable policy given your situation and adjust it as necessary.

The amount of life insurance you get depends on numerous factors and varies significantly from person to person. Here are a few tips to help you determine how much life insurance you should get.

The amount of life insurance you need will depend on your personal financial situation. Start with these three factors:

Thinking of life insurance as part of an overall financial plan helps you anticipate what finances you should cover in your policy. Consider future expenses, kids’ college tuition, inflation, future asset growth and more.

It’s typically best to opt for more coverage to leave a cushion for increasing financial needs over the years. For example, inflation could increase the cost of living. In these situations, a little extra coverage would help to ensure your family could continue to live comfortably.

If it’s a challenge to determine how much life insurance you may need, consider speaking to a financial advisor or trusted insurance agent. These experts can help you weigh your options and determine the amount of life insurance for your situation.

People use numerous methods to estimate how much life insurance they need. Some people say to multiply your income by five, seven or even 10 to get a starting point. Others say to add an additional $100,000 per dependent on top of that to account for college and other living expenses.

These methods are great for determining a starting point, though your financial situation could include various other needs that could change how much coverage you need. It’s best to include as many factors as possible to get an accurate calculation.

Some methods, like the DIME formula, consider a few more financial aspects that we mentioned above:

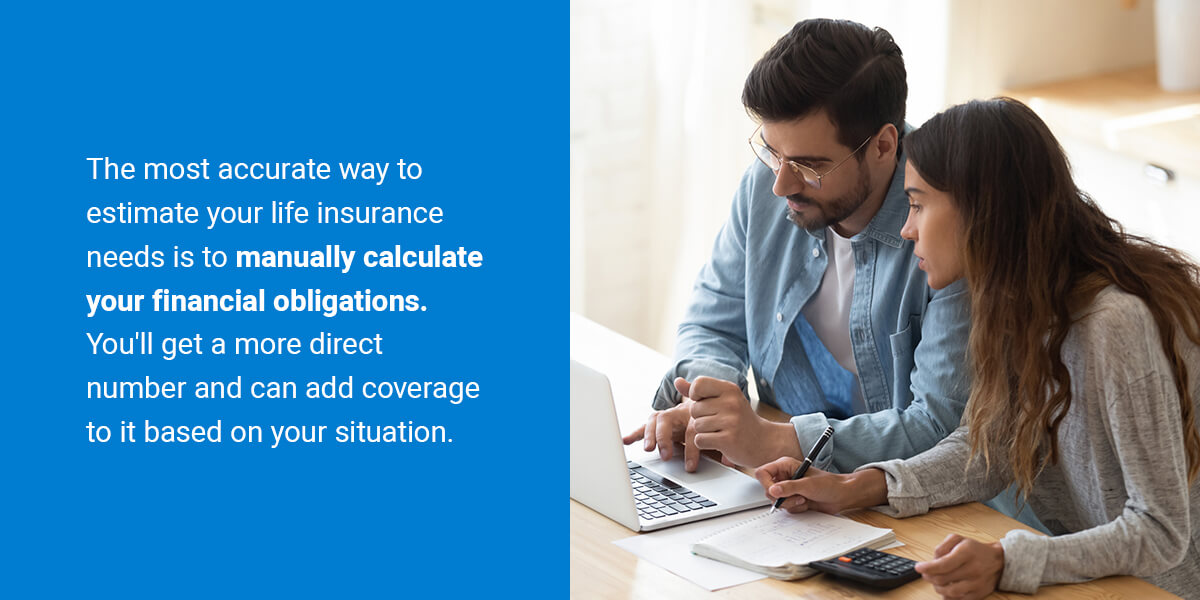

Add up all these financial obligations to get a closer estimate of what you may need in life insurance. The most accurate way to estimate your life insurance needs is to manually calculate your financial obligations. You’ll get a more direct number and can add coverage to it based on your situation.

Determining your life insurance needs can be confusing and requires a lot of consideration. You’ll likely have many questions along the way, which will help you understand your policy thoroughly.

Here are some frequently asked questions that can help you better understand your life insurance policy and how much coverage to get.

Permanent life insurance policies have cash value aspects, which can be used as an investment. Policies with a cash value allow you to save money that gains interest, which you could use for retirement or other savings.

When considering a life insurance policy as an investment vehicle, it’s important to consider potential returns and how disciplined you are in investing.

Most insurance companies require a physical exam, though some companies will provide policies without requiring one. The physical determines how much of a risk you are to insure for the insurance company, which can in turn affect your premium. Insurance companies that don’t require a physical typically have more expensive life insurance policies.

Your life insurance beneficiaries are the people who receive your death benefit. While most people name their family members as beneficiaries, you can ultimately name anyone as a beneficiary.

If you have a permanent life insurance policy like a whole or universal policy, you may come across the term “fully paid up.” This refers to paying enough premiums that you no longer have to make payments. When your policy is fully paid up, you’ve covered the cost of insurance for the remainder of your life.

What happens to the cash value depends on the terms of your policy. Some insurance companies pay out the cash value in addition to the death benefit. More often though, insurance companies only pay out the death benefit and the cash value goes back into the insurance company.

The amount of life insurance you need depends on your financial situation. Consider factors like your debt, dependents, income and other financial needs your loved ones would have in your absence. Talk to an insurance expert for help determining how much life insurance you should get.

Deciding on a life insurance policy can be challenging, but you don’t have to do it alone. At David Pope Insurance, we’ll help you find an affordable life insurance policy that best suits you and your family’s needs. Contact our team online or call us at 636-583-0800 for help determining how much life insurance to get. Request a quote for a life insurance policy today.