Our insurance needs change over time. Despite this, many consumers stay with the same insurance provider for years. By changing insurance companies, you can find policies that meet your current needs and potentially pay lower premiums. If your insurance needs have recently changed or you’ve been with the same carrier for years, now may be a good time to review your policy and look for discounts or shop around for better prices.

Are you in need of tips for switching insurance? We’ve compiled a list of tips and tricks so you’ll know precisely how to change insurance.

Jump To:

Before your renewal period, browse for competitive insurance rates and research the incentives your current carrier offers to ensure you’re not paying more than you need to. If you’re planning to switch your insurance, the best time to make the switch is before your renewal.

Below are reasons you should consider switching your insurance, whether you’re looking for more comprehensive coverage or need to save more each month on your premiums.

Without enough coverage, you could leave yourself exposed financially. On the other hand, you’ll be spending more than necessary if you have too much coverage.

If you’re switching car insurance and you drive an older vehicle, maybe you’ll decide you don’t need to have collision and comprehensive coverage. Another option may be choosing a policy with a higher deductible so you can save money.

To determine your coverage needs, consider how much you need to protect. If you’re fresh out of college, renting an apartment and don’t have many assets, you may not need the same amount of liability coverage as a homeowner who has multiple vehicles and a large savings account.

If you want to obtain additional insurance, find less restrictive coverage or drop any coverage you don’t need, this is when to change insurance.

For auto insurance, in particular, switching to a different provider can save you a lot of money on your premium. Mentioning that you’re in the market for new insurance to your current provider can also save you money, as your current company may offer a better premium and additional discounts so they can keep your business.

If you’re considering switching homeowners insurance, you may find a better price when you shop around, even when you take into account any loyalty discounts you may be entitled to.

Additionally, if you bundle your home insurance and auto insurance, you may be able to save money. If your policies are with different providers, you may want to consider switching one of your policies so they are both under the same company.

Moving out of your insurer’s territory is another reason to switch insurance providers. Several companies provide insurance only to residents in certain states. If your current provider doesn’t service the state you’re moving to, now is the time to begin looking for a new provider.

Another reason you may want to work with a different insurance company is if you’ve dealt with poor customer service from your current provider. Maybe you’ve previously had to file a claim, and your insurer was challenging to work with. Maybe you’ve found reviews from other customers who also complain about poor customer service. In this case, you may want to find a different company that provides higher-quality customer service.

Another major reason you may want to switch insurance is if you’re anticipating a major life change or a major life change. Significant life changes can include getting married, having a child, purchasing a car or home or adding another person to your policy.

For example, if you’ve bought a house, you’ll want to shop for insurance once the seller accepts your offer on the house. You want to be proactive about securing the right insurance for your new home because this is likely one of your most significant assets, if not the largest, and you need to ensure it’s protected.

Now that you know why to change insurance policies, you may want to analyze what insurance coverage you need. If you have auto, home and life insurance, you may want to look at each of your policies. Have your coverage needs changed since you purchased the policy? Are your current policies still meeting your coverage needs? If not, now is the time to determine exactly what coverage you need.

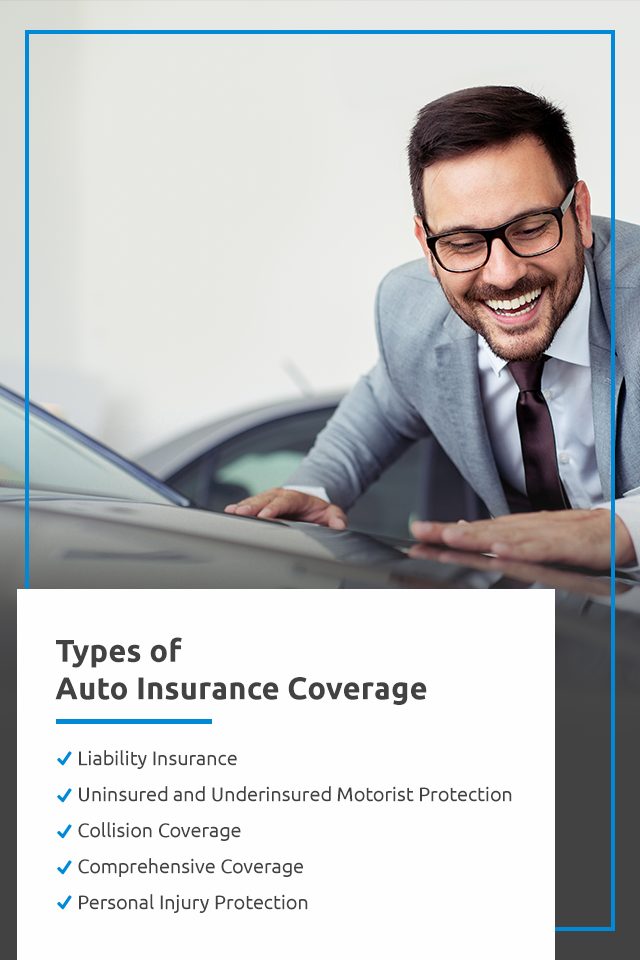

The following is a list of common types of auto insurance coverage:

Liability insurance for your vehicle covers you if you cause a car accident. It is required in most states. This type of insurance is divided into property damage liability and bodily injury liability.

In most states, drivers are mandated to have at least a minimum liability insurance, though you generally want to secure more than the minimum if you can afford it.

Having more than the state’s minimum required liability insurance gives you an additional buffer should you be deemed to have caused an accident. You will be responsible for claims that exceed the limit of your coverage. You’re taking a major financial risk by keeping your coverage at the minimum requirement.

Not every driver is insured, despite what state laws mandate. If you’re in an accident with someone who doesn’t have adequate insurance to cover the damages you suffer from an accident, you may not receive all the payment you need. In this instance, Uninsured and Underinsured Motorist Protection can assist you with these costs. This coverage is also quite affordable, especially for the protection it offers you.

Collision coverage pays for your vehicle repairs in case of a covered accident. Say you get into an accident, and your car is totaled. If the cost of repairs is more than your car is worth, collision coverage will pay you your car’s value.

Do you have an older car? If so, maybe the low value of the car means it isn’t worth insuring with collision coverage. On the other hand, a more expensive or new car should be insured with collision coverage so you can get your money back after your car gets damaged.

Your car may also suffer damage caused by incidents such as theft, weather damage or hitting a deer. These kinds of damage are what comprehensive insurance will cover. If comprehensive coverage fits your budget, you may want to include it in your policy.

You may want to forgo comprehensive coverage if it’s out of your budget and your car can be easily replaced. If you want to include comprehensive coverage in your plan, installing a tracking or anti-theft device may help you make your coverage more affordable.

You will likely want to secure Personal Injury Protection if available. This covers the medical bills you or your passengers may be saddled with after an accident, no matter which driver is deemed to have been at fault. Personal Injury Protection isn’t available in every state, so check which coverages are available in your state before switching insurance companies based on this lack of coverage.

There are standard coverages usually included automatically and several optional coverages for homeowners insurance policies.

Standard coverages for homeowners insurance include:

This pays out for others’ injuries if those injuries occur on your property and you’re found responsible.

This helps cover repairs to damaged belongings and replacements for stolen belongings in a covered loss. These belongings can range from your dishes to your furniture.

This helps cover the damage your home sustains and any attached structures, like a garage.

This helps cover damage to stand-alone structures, including structures like tool sheds, fences or carports.

This helps cover the costs for treatment of injuries for guests on your property or for an individual you or a family member accidentally injure when you’re away from home. This coverage is applicable no matter who is found to be at fault.

This helps cover a temporary relocation along with your basic living expenses, such as your meals, if a loss covered by your policy forces you to leave your home during repairs. This coverage is also referred to as “loss of use.”

Optional coverages for homeowners insurance include:

This coverage is available if you find that your initial coverage isn’t enough or the construction cost unexpectedly increases. Enhanced dwelling protection prevents you from pulling from your savings to cover the costs of rebuilding your home.

This coverage exists for the high-end belongings in your home that exceed standard personal property limits. This may include items like fine art and jewelry.

This helps cover the costs of damages caused by a burst pipe or another plumbing issue. Some insurers include this coverage automatically. This coverage does not apply to flash floods.

This helps cover expenses you may face after becoming a victim of identity theft. Your insurer may also include assistance from an advisor on identity theft in this coverage. This advisor can deal with bill collectors and creditors to restore your credit.

Lastly, there are two main types of life insurance coverage:

Term life insurance, or temporary insurance, is issued for a several years. This term often ranges from five to 30 years.

Theoretically, permanent life insurance, also known as whole life insurance, covers you for the duration of your life. There may be an expiration at a certain age, generally when the policyholder hits 100 years old.

Familiarize yourself with the common types of coverage for the insurance you seek so you know what coverage is necessary for you and what isn’t. There are different types of permanent life insurance policies you can choose from, including:

Depending on your individual needs, you may choose one type of permanent life insurance policy over another.

Supplemental life insurance is typically connected to your employment, and the policy length varies between employers. Some policies will be term length, while others may be permanent.

Because this life insurance is connected to your work, you can receive it for little to no cost, and rates are set based on the group rather than the individual. The death benefit for supplemental life insurance is also fixed. Supplemental life insurance is generally a good addition to your existing life insurance policy, whether you choose term based or permanent.

While these insurance policies can be an ideal addition, there are a few downsides. For example, if you lose your job or change careers, you’ll also lose the supplemental life insurance policy. This is why it’s ideal to have your own insurance that’s not tied to your employment and use this type of insurance as a supplement. When you buy your own policy, you can choose better insurance policies to cover your needs.

You may have an existing insurance policy but want to look for something better or more in-depth to cover your car, home or life. If you’re considering or preparing to switch insurance, you should consider a few things to ensure you pick a policy that works for you. For example, you’ll want to talk to multiple agents to get an idea of the best policy, review your quote to ensure your coverage and take the proper steps to switch your insurance.

Below, you’ll learn more about how you can switch your home and car insurance and cancel your old policy, ensure you’re always covered and get the most out of your coverage.

If you can, research a month or two before your policy’s renewal. Auto policies, for example, typically last for six months or a year. Doing your research well before the renewal date will allow you to take your time and make the most informed decision by comparing as many carriers as possible.

When you’re shopping around, ask about the discounts and benefits offered. Not all insurance agents are created equal — find one that has your best interests in mind and gives you sound advice. You may think a lower car insurance quote may save you money, but it may not have all the benefits you need, or it may include benefits that aren’t useful to you. Ask about what would be covered under the new policy and how much protection you would receive.

Compare rates from multiple companies to ensure you get the best deal for the coverage you need. For auto insurance, acquiring a minimum of three quotes should give you an idea of the coverage standards and average costs.

You should also thoroughly research an insurance provider before making the switch. You may be able to find information about the customer complaint ratio and find reviews from other customers online. You may want to call them to get a sense of the quality of their customer service.

The cost of your premium isn’t the only factor you should consider when selecting a provider. You want to work with an insurance company that cares about its customers and won’t be challenging to deal with if you need to file a claim.

Talk to your current insurance provider as well. If you let them know that you’re shopping around for a better deal, they may offer you a better rate to keep you as a customer. This is also an excellent time to check for any discounts you may miss out on at your current provider. Ask about how a driver’s education course may lower your premium. If you’re a student, mention your GPA. If you have a shorter commute, ask if your lower mileage can get you a lower premium.

If you decide to switch your insurance, follow the proper steps. These steps are:

Below, we’ll provide more details about how to switch your insurance policy, including how to review your insurance quote, notify your lender that you’re switching insurance policies and cancel your insurance policy.

After you receive your quote, make sure you review it carefully. For example, the following information and factors will typically affect your quote when you’re changing car insurance:

Drivers can also commonly save money by bundling their car and home insurance.

Discuss your quotes with insurance agents from each carrier deciding so you know exactly what benefits and discounts are available to you.

Many homeowners pay their homeowner’s insurance premiums through an escrow account. This means that your lender uses part of each mortgage payment you make to pay for your insurance and other costs, such as property tax. If you have an escrow account, you don’t have to worry about making your homeowner’s insurance payments — your lender handles this for you.

If you currently pay your premium by escrow and you’re thinking of switching your homeowners insurance policy, though, it’s essential that you let your lender know. Notifying them enables them to ensure that your payments go to the right company. Your lender will need your permission to communicate with your insurance agent. Your new insurance agent will require your loan number, previous policy number and social security number so that they can work with the lender.

Let your lender know as soon as possible that you’re planning to switch your homeowner’s insurance. Ideally, let them know before you switch.

If you decide that switching insurance is the right choice for you, the next question is — can you cancel your insurance at any time?

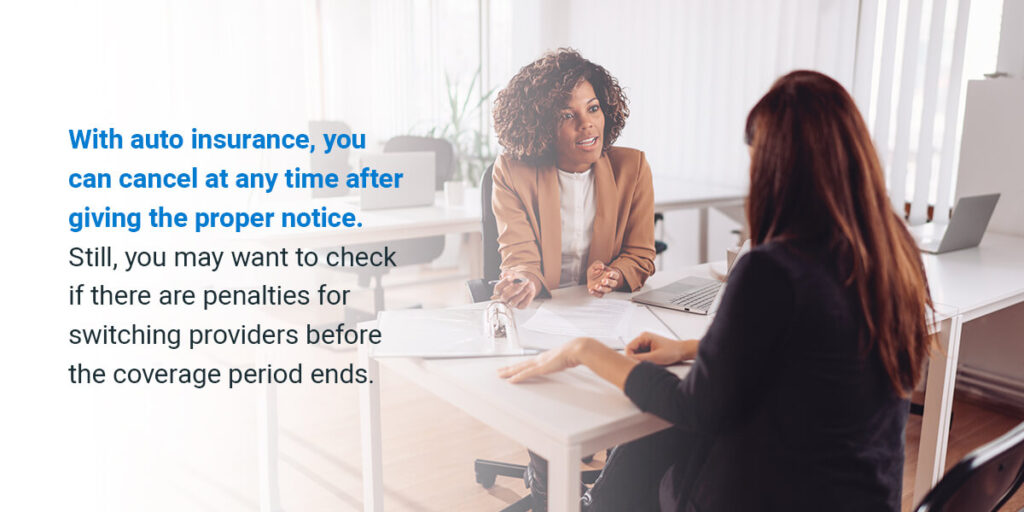

With auto insurance, you can cancel at any time after giving the proper notice. Still, you may want to check if there are penalties for switching providers before the coverage period ends. Most auto insurance companies will refund unused premiums but may charge a fee to customers who cancel car insurance in the middle of the policy term.

If you’ll be penalized if you cancel your car insurance early, crunch the numbers to determine whether you should switch insurance now or after your policy expires.

When you’re switching insurance, there are a few steps you’ll want to take and some important notes to keep in mind before you cancel your policy. Stopping monthly payments isn’t enough for policy cancellation. In fact, this could hurt your credit if your provider reports you for non-payment to the credit bureaus.

First, do not cancel a policy until the new one is purchased and active. Policies start at 12:01 AM on the date you issue. By waiting to cancel until your new policy is active, you’ll avoid a coverage gap.

Ensure you cancel your old policy after the new policy is in effect, and check to make sure the old company reimburses you for payments already paid that are due back to you. If you paid for a half-year policy for auto insurance and decide to switch companies after three months, for example, your provider will likely reimburse you for those remaining three months of coverage.

If getting your refund is a hassle, you should handle this issue as soon as you cancel your policy. If there are further delays on reimbursement, follow up with your previous insurer.

We’ve answered some common questions below in case you have lingering questions, thoughts or concerns about switching insurance providers.

Yes, it’s still possible to switch your car insurance if you have a loan on your vehicle. If you need a new insurance policy to find the right coverage within your budget, it’s more than possible to make the switch. Remember to list your lender as an interested party in your insurance policy to ensure your lender knows you have the required coverage.

There are some cases where you could switch insurance with an open claim, but ideally, you’ll want to wait until the claim closes. If you have a claim open when you switch, you may have an expected premium change if your risk profile changes after the claim close.

The answer to this question varies for everyone. Instead of considering how often you should switch, you should compare different insurance policies to ensure you’re getting the best deal with your current insurance provider.

Even if you shop around, it doesn’t mean you have to switch — you may be happy with your current insurance policy. Ideally, you’ll only want to change if you’re not happy with your policy or if you want to find a policy that fits within your budget.

If you’re looking to switch insurance and want to find high-quality coverage at a price you can afford, look no further than David Pope Insurance Services, LLC. At David Pope, we review every policy at the time of renewal to help guide our customers to the best possible coverage for their lifestyle.

Whether you’re in the market for auto insurance, life insurance or home insurance in Missouri, we provide affordable rates for the coverage you need at David Pope Insurance. Request a quote from us today or contact us to learn more about how you can get the most from our insurance coverage.