For homeowners, home insurance is a necessity. This insurance protects your home and your belongings from theft or damage, and almost all mortgage companies mandate that borrowers have home insurance coverage for the fair or full value of their property. Without proof of home insurance, many mortgage companies will not finance a real estate transaction.

Many homebuyers may not know what to look for when it comes to home insurance comparison. Are you looking to understand the cost of your quotes or get cheaper quotes? Maybe you want to better analyze the numbers from a home insurance comparison tool. At David Pope Insurance Services, LLC, we have compiled this guide to help you understand how to compare home insurance quotes so you can feel confident in your decision.

Jump To:

Homeowners insurance policies are highly customizable, but they also include standard elements that determine what costs are covered by the insurance provider. Some of the key areas covered may include:

Your home insurance’s liability coverage is intended to protect you from lawsuits filed by other people. This liability coverage includes your pets, which means if your dog bites a neighbor, your insurance provider may pay for the neighbor’s medical expenses. If someone is injured while on your property and they sue you, you may also be covered.

To obtain a significant amount of liability coverage at an affordable rate, you may want to consider an umbrella insurance policy.

The interior or exterior of your home can be damaged by covered disasters, such as hurricanes, fire, lightning or vandalism. In these situations, home insurance may cover the costs if your home needs repairs or needs to be completely rebuilt. Belongings like appliances, furniture and clothing may also be covered if destroyed by an insured disaster. To cover lost jewelry, you can obtain off-premises coverage.

How much your insurance company will reimburse you for interior or exterior damage to your home may be a limited amount. For example, if you have coverage for 70% of your amount of home insurance and your home is insured for $150,000, you may have coverage for $105,000 worth of belongings. If many of your possessions are high-priced items, such as designer clothes, fine jewelry or fine art, you may want to pay more for coverage of these belongings.

If you are ever forced to live out of your home temporarily due to home repairs or reconstruction, additional living expenses coverage may reimburse you for a hotel room or rent, restaurant meals and other costs you incur. Keep in mind that your policy will likely impose daily and total limits for what will be reimbursed while you are out of your home. If you want to increase these limits, you can pay more for coverage.

Home insurance covers many scenarios where a loss could occur, but not all events will be covered. Typically, events that are excluded from most home insurance policies are natural disasters, acts of war and acts of nature not included under covered disasters. Common exclusions from home insurance include:

For many of these exclusions, you may be able to purchase additional or separate coverage to get the protection you need. For example, if you want protection in the event of a flood, you can obtain a separate flood insurance policy. You may also consider adding sewer and drain backup coverage.

While you may have coverage for certain dog breeds, others may be excluded if the risk for that breed is too high. If your dog is an excluded breed, you can purchase additional coverage. You may also want to purchase separate coverage for the other structures on your property, such as a shed or a freestanding garage. If you are concerned about identity theft, you can purchase identity recovery coverage for protection.

Insurance companies determine quotes by assessing risk. To accurately compare home insurance rates, you may want to know which factors influence your quotes. The following are some factors to keep in mind:

With so many factors contributing to a home insurance quote, shopping around for the right policy can be a good option if you’re trying to save money. Reference the considerations above as you compare home insurance costs. Remember that while a good rate quote is excellent, you’ll also want coverage that adequately suits your lifestyle and needs and quality customer service.

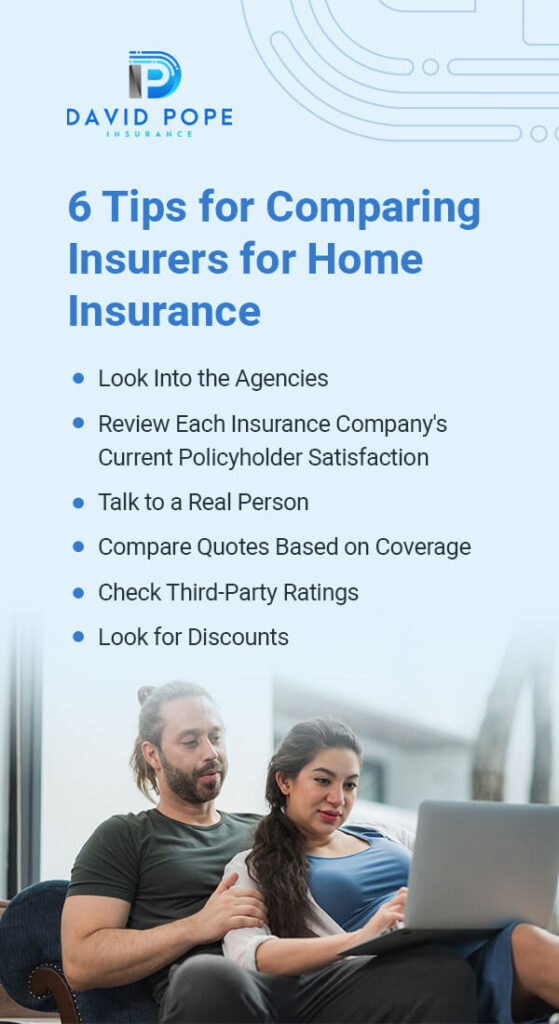

Although shopping around for home insurance quotes can feel time-consuming, it’s beneficial in the long run. Searching for the policy that best fits your unique coverage needs can help you save a significant amount of money by not over- or under-insuring your home. To compare home insurance plans and insurers, you may want to look into the agencies, review current policyholder satisfaction and talk to a real person at the company:

First, you want to make sure the agencies are legitimate and worth your time. You can check the health of home insurance companies by considering the scores available on the websites of top credit agencies. Look for customer feedback and consumer complaints that may have been made against these companies. You may also want to know how a company processes claims.

Before you choose to work with an insurance company, you may also want to consider the insurer’s claims response. How long will you be in a difficult financial position if you suffer a large loss that you need to pay for out-of-pocket while you wait for reimbursement? Prior to purchasing a policy from an insurer, you may want to find out who will be receiving and handling claims calls.

When you compare homeowners insurance rates and companies, your next step is reviewing current policyholder satisfaction. Though every insurer will say it provides good claims service, you may want to ask an insurance agent about the company’s retention rate. This is the percentage of policyholders who renew their policies with the company each year.

Additionally, you can find information about policyholder satisfaction in online reviews, testimonials and annual reports. If you have friends or family with policies at an insurance company, you can ask them about their satisfaction with the insurer.

Often, the best way to get the most accurate quote and gather more information about an insurance company is to speak directly to an insurance agent who works with several insurers. These agents tend to be more transparent than captive agents who work for a single insurance company. At David Pope Insurance, we provide exceptional customer service and can answer your questions about the right home insurance policy for you.

Home insurance companies may use different factors when determining a quote and charge different rates for varying coverage amounts. If possible, compare policies that offer the same amount of coverage. Comparing policies by coverage rather than price will help you tell which insurance company charges the most affordable rates for what you need.

It’s vital to remember that the cheapest isn’t always the best — a surprisingly low-cost policy may not offer the coverage you need. The best insurance policy is one that fully covers your home and belongings.

Policyholder satisfaction can tell you about an insurer’s customer service and whether their coverage fits policyholders’ needs. However, those considerations are only part of the larger picture. It’s also beneficial to check an insurer’s third-party ratings for financial strength. An insurer’s financial stability is essential for people considering homeowners insurance.

Insurance companies receive ratings from third parties like Standard & Poor’s (S&P) and AM Best. These third parties determine an insurance company’s financial stability by calculating:

You may be able to find these ratings on an insurance company’s website.

Most insurance companies offer some form of discount for home insurance. For example, many insurers allow homeowners to bundle their home and auto insurance for a lower monthly rate. You may also be able to save if you pay your annual premium in full or install a home security system. Discounts vary between insurers, so check with each to see what they offer and whether you qualify.

Home insurance comes in several policy forms. Some policy options provide more coverage than others, which is why it’s important for homeowners to know the difference. Though details tend to differ by company and state, the following are the standard homeowners insurance policy options:

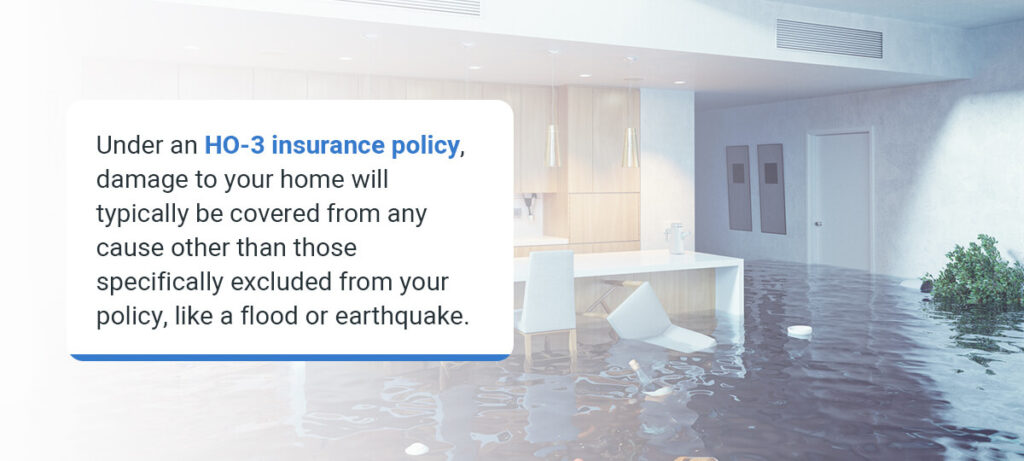

An HO-3 insurance policy is also referred to as a special form policy. This type of policy is the most common. If you are a homeowner with a mortgage, your lender likely requires that you obtain at least this level of home insurance coverage.

Under an HO-3 insurance policy, damage to your home will typically be covered from any cause other than those specifically excluded from your policy, like a flood or earthquake. Unless you purchase additional coverage, your belongings will likely only be covered from the following named perils:

Less popular policy options are HO-1 and HO-2 home insurance policies. These policies only cover damage that was caused by an issue listed. Under an HO-2 insurance policy, your house and belongings typically will be covered only if damaged by the perils listed above. HO-1 insurance policies are less widely available and are the most basic home insurance policy types. This policy type covers even fewer perils than an HO-2 policy.

HO-5 insurance policies are also referred to as premier coverage or comprehensive form coverage. These policies provide the broadest home insurance coverage. Besides the causes that are specifically excluded, this policy typically covers the damages from all causes. Not all insurance companies offer this policy option, and it is generally only available for homes that are well-maintained and located in low-risk areas.

Keep in mind that HO-3 policies are sometimes labeled as “premier,” but they don’t offer the broad coverage found in an HO-5 policy. Speak to your insurance agent if you want an HO-5 insurance policy.

In addition to the previously covered types, other homeowners insurance policy types include:

How much home insurance you will need depends on how much it will cost to rebuild your home if it gets destroyed. When you set the dwelling coverage limit for your home insurance policy at the cost of rebuilding, you can rest assured you will have enough coverage for repairs and you also won’t be paying for coverage you don’t need.

To calculate your estimated rebuilding cost, you can multiply the square footage of your house by the costs of local construction per square foot. Your insurer or insurance agent may be able to help you estimate the cost of home replacement. To determine how much coverage you need for your personal property, you may want to take an inventory of your belongings.

As you compare home insurance costs, you may find that you want to add to your coverage beyond the most common policy options. Many insurance companies offer a range of add-ons and separate policies that plug gaps in coverage. Here are a few to consider:

If you want a home insurance quote, you may need to provide the following information:

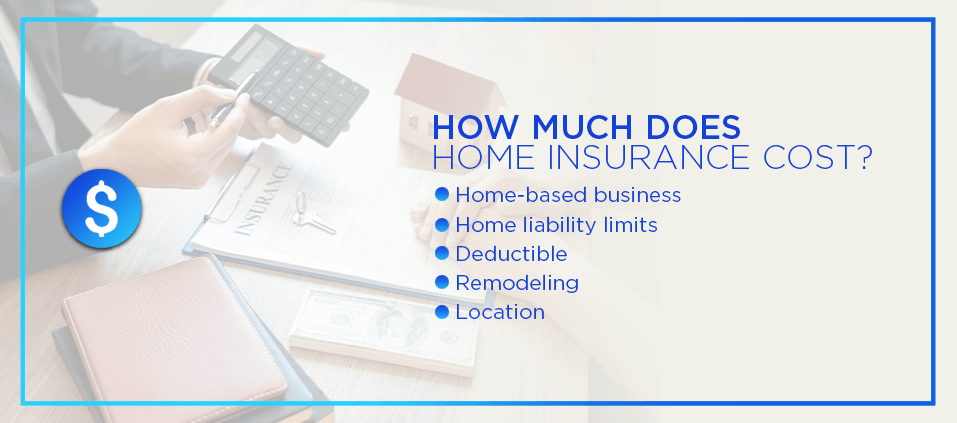

On average, home insurance costs a few thousand dollars every year. This figure considers factors including:

The following are additional considerations that determine your home insurance costs:

When determining how to calculate home insurance costs, it’s important to note that just getting a quote could be one of the first expenses. Luckily, there are ways around that. Here are a few tips for getting a discounted or free home insurance quote:

Cost-Cutting Insurance Tips

Cost-Cutting Insurance TipsYou may be able to cut costs from your home insurance by following these tips:

At David Pope Insurance, we offer our clients financial stability by finding the lowest rates for homeowners insurance available on the market. With more than 20 years of experience and 15 years in the business, our insurance firm is local and family-owned. We provide Missouri residents with the following types of insurance:

If you want to obtain insurance that will give you peace of mind while also keeping your costs low, we can provide the liability coverage you need to protect your assets. When you choose David Pope Insurance, we’ll provide a fast, flexible quote that is customized for your specific insurance needs. Let us know about your unique situation, and we can help you find the right coverage for the best premium possible.

Request a free quote for home insurance in Missouri or contact us at David Pope Insurance today.