When choosing a home insurance policy, your house is the main priority. However, you should consider your property as a whole — including your yard and unattached structures. Yard damage can happen anytime, and many homeowners must fix issues out of pocket.

Explore whether home insurance covers yard damages and the specific hazards your policy may cover.

Yard damage refers to the destruction of or harm to any external structures and contents on your property that are not attached to your house. Under most homeowners insurance policies, yard damage is covered by “other structure” insurance, also known as coverage B. Insurance companies pay claims after you have paid your deductible.

Outdoor structures your homeowners insurance policy might cover include:

While coverage B typically covers these outdoor structures, not all policies do. Be sure you know what your specific policy covers. Covered perils are damages your insurance company will cover. For yards, covered perils often include.

Homeowners insurance may cover landscaping such as trees, plants, gardens, shrubs and lawns under a covered peril. Learn more about how trees and erosion affect your insurance coverage.

While trees fall under landscaping, specific conditions influence whether you can file a claim. For example, if a tree falls on your outdoor structure due to wind, your homeowners insurance will pay to remove the tree and repair the damages. However, if a tree falls over and no structure is harmed, you cannot make a claim to have the tree or stump removed.

If a neighbor’s tree damages structures in your yard, you might be able to file a claim with your insurance or theirs. Some policies also cover healthy trees uprooted by certain conditions. However, if a weak and rotting tree breaks, insurance usually won’t cover any damage the falling tree causes.

Erosion is often due to water damage from pipe bursts and floods, leading to weak foundations and earth displacements. Home insurance usually does not cover erosion caused by weather conditions. However, if other structures covered in your policy are damaged by erosion, you might be able to file a claim. It’s best to get insurance add-ons to help you cover erosion damages.

Standard policies typically cover common perils and outdoor structures. However, specific cases could compel you to get additional coverage or pay extra costs. Consider these examples of yard damage:

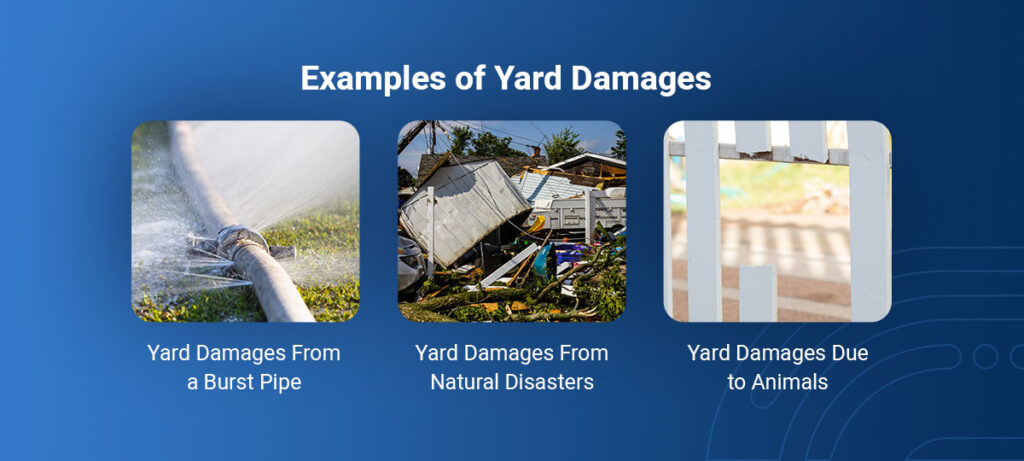

Debris build-up and wear can cause pipe bursts in yards, and a burst pipe can cause water damage and erode outdoor property. A home insurance policy will likely cover a burst pipe if the cause is included in the covered perils. However, there is no coverage if a pipe bursts due to a lack of regular maintenance.

Weather conditions such as high winds, snow, lightning, storms and hail are likely covered. Some insurance companies and policies also cover hurricanes, tornadoes and volcanic eruptions.

However, homeowners insurance generally does not cover natural flooding caused by dam failure, rivers, heavy rainfall and earthquakes. If you live in a high-risk location, get coverage for earthquakes and flooding with additional policies that accommodate these hazards. Homeowners insurance also doesn’t cover standard wear and tear from regular weather.

You can likely file a claim when a larger animal damages an outdoor structure. However, homeowners insurance does not cover smaller animals, like rodents, birds and insects.

When getting home insurance, ensure that your yard and other structures are covered. Find out what your standard policy covers and how much coverage you will receive. There are many different types of home insurance policies. Some offer specific coverage, whereas others give full coverage for repair or replacements.

It helps to be prepared for costly damages or liabilities. Here are the steps to follow when claiming yard damages:

Some insurance might deny your claim even if you have proof of damages. Claim denial can cause disputes and delays. Even if you get an offer, it might not be enough to cover costs. It’s best to take pictures and get descriptions of your outdoor structures when you get your insurance to show their condition before the incident. Having documents to refer back to will help substantiate your claim.

Some damage isn’t covered by a covered peril. When that happens, it is the homeowner’s responsibility to pay for repairs and replacements.

Contact Us Today!Home insurance policies typically do not cover specific perils or damage due to certain conditions. For example, if you use your outdoor structure for a commercial business, it should be covered by business insurance. Additional hazards not covered include:

If your yard does sustain damages, a few factors may prohibit you from making an insurance claim:

Insurance policies generally do not cover preventable negligence by the homeowner. For example, maintaining structures and addressing issues could limit covered perils such as frozen pipes and water damage. With preventative measures in place, you stand a better chance of claiming insurance and creating a safer space. Get Yard Coverage With David Pope Insurance Services, LLC

Get a Free QuoteGetting the right home insurance is essential to ensure your yard and outdoor structures are secured in the event of a covered peril. Many factors influence whether you can file a claim, so you must do extensive research to choose one that provides adequate yard coverage.

At David Pope Insurance, LLC, we provide peace of mind to our clients, knowing that their assets are covered. We have over 20 years of experience in the business and offer clients expert advice and the lowest rates for auto, home and life insurance.

To contact us, complete an online form or request a quote today. Our representative will get back to you shortly.